You need to avoid late BAS payments.

Managing the responsibilities associated with running a business has never been more extensive or demanding than it is today. One very important aspect that sometime gets overlooked is the Business Activity Statement (BAS) lodgements and payment.

The Australian Taxation Office (ATO) is now returning to pre pandemic collection activities as the small business debt increased from $26.5 billion in 2019 to $50.2 billion to 2023 and unpaid super at $2 billion.

In its address to the Tax institute in September 2023 the ATO detailed its firmer action policy and willingness to escalate to legal action and if necessary apply for the liquidation of a company where companies fail to reconnect, lodge and pay on time.

It is now more critical than ever to ensure that your BAS reporting and tax affairs are in order. If you’ve submitted a late BAS statement, here’s what you may want to consider.

BAS due dates

Business Activity Statements (BAS’s):

Quarterly BAS due dates

Quarterly BAS’s are due 28 days after the respective BAS period (e.g., March 2023 Quarter BAS’s are due on 28 April 2023). If lodged through a BAS agent, you are granted an extended due date of the 25th day two months after the respective BAS period (e.g., March23 Quarter BAS’s are due on 26 May 2023).

Monthly BAS due dates

Businesses lodging Monthly BAS’s must submit them by the 21st day following the BAS period and do not receive the extended due date concessions granted to Quarterly lodgers. If you currently lodge BAS’s monthly and want to switch to quarterly reporting for convenience and extended lodgement periods, you must have a sales turnover of less than $20 million and contact the ATO to make the change unless they’ve mandated monthly lodgement for other reasons.

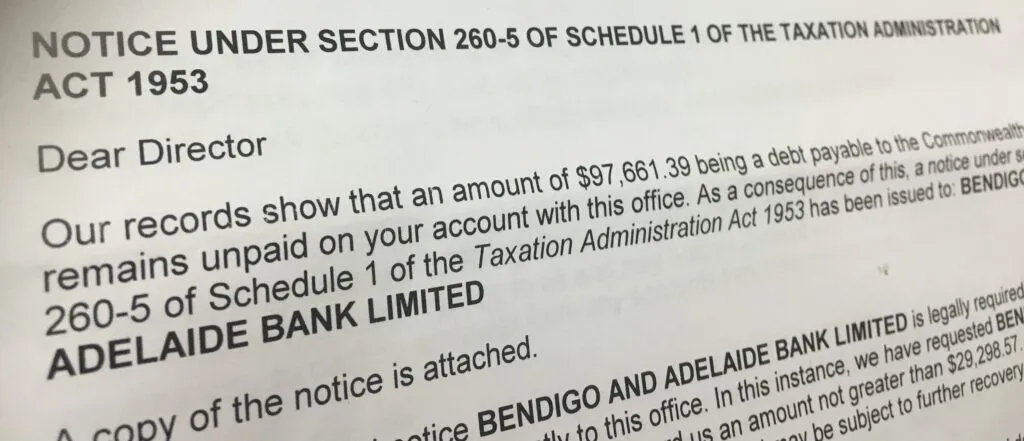

Director Penalty Notices

If you lodge your BAS late and the amounts remain unpaid the ATO can issue you with something call a director penalty notice. These notices have an expiration date of 21 days that can make the director of the company personally liable for company debts.

If you receive a DPN please contact us or your accountant or a lawyer.

What happens if you pay BAS late?

ATO Penalties and General Interest Charges

1) Breaching any of the due dates mentioned above can subject you to the ATO’s penalty system, which issues Penalty Units (currently $210 per unit) based on the violation and outstanding period. ‘Failure to lodge’ penalties are calculated according to the entity’s size and each 28-day period the tax return or BAS statement remains overdue.

2) ‘Small Entities’ with a turnover of less than $1 million receive one penalty unit per period overdue, capped at a maximum of five penalty units, or $1,050.

3) ‘Medium Entities’ with a turnover of $1 million to less than $20 million or PAYG withheld amounts totaling between $25,001 and $1 million in a previous year (medium withholders) receive two penalty units per period overdue.

4) ‘Large Entities’ with a turnover of $20 million and above or PAYG withheld amounts totaling $1 million in a previous year (large withholders) receive five penalty units per period overdue.

5) Additionally, the ATO applies a general interest charge (GIC) for any unpaid tax liability or BAS statements from the due date until the amount is settled, including associated penalties and interest charges.

You’re Late – What to do now?

If you faced extenuating circumstances that affected your ability to lodge (e.g., natural disasters or serious illness), you can apply to have the penalties and interest charges waived. However this is becoming more difficult.

If neither of the above applies, you should promptly lodge and pay your Income Tax Return or BAS Statement, including any penalties and interest. If immediate payment is not feasible, consider entering into a payment arrangement with the ATO, which can mitigate or reduce your penalty consequences, though general interest charges will still apply.

This is not accounting advice and you should speak with your accountant for advice.

Are you eligible for Small Business Restructuring?

If your business is under financial stress and suffering from tax debt, a Small Business Restructure may be a good solution.